Home » How to Refinance Your Home Loan in Australia and Save Thousands on Your Mortgage

Did you know that staying loyal to your bank could be costing you thousands of dollars a year? If you haven’t reviewed your mortgage in the last 12 to 24 months, there’s a good chance you are paying more interest than necessary. Whether you’re looking to consolidate debt, access equity for renovations, or simply secure a lower rate, deciding to refinance home loan Australia-wide is one of the most effective financial moves you can make.

In this guide, we’ll walk you through everything you need to know about switching lenders, understanding the costs involved, and why getting expert advice from a local broker can make all the difference.

Refinancing is simply the process of replacing your current mortgage with a new one. This usually involves switching to a different lender, although you can sometimes refinance internally with your existing bank.

The goal of home loan refinancing is to secure a loan that is better suited to your current financial situation. When you refinance, your new lender pays off your old loan, and you begin making repayments on the new loan—ideally with better terms.

For many Australians, the motivation to refinance mortgage Australia markets offer is driven by a desire to reduce monthly overheads or to access features that weren’t available in their original loan package, such as offset accounts or redraw facilities.

The primary reason most people switch is to save money. Even a small drop in your interest rate can have a massive impact over the life of a 30-year loan.

Lower Home Loan Interest Rate: If your current rate is 6.5% and you refinance to a rate of 5.9%, the difference might seem small, but it compounds significantly.

Reduce Mortgage Repayments: A lower rate directly lowers your monthly repayment obligations, freeing up cash flow for other living expenses or savings.

Debt Consolidation: By rolling high-interest debts (like credit cards or car loans) into your home loan at a much lower interest rate, you can reduce your total monthly outgoing payments.

Timing is everything in the property market. While there is no single “perfect” time, there are specific scenarios where it makes financial sense to look at your options, particularly if you are looking to refinance mortgage Sydney-wide or in regional NSW.

Rising Interest Rates: When the cash rate climbs, banks pass this on to borrowers. Refinancing can help you find a lender who is more competitive in a high-rate environment.

Improved Credit Score: If your credit score has improved since you first bought your home, you may now qualify for “tier-one” loans with significantly lower rates.

Increased Property Value: If your home in NSW has increased in value, your Loan-to-Value Ratio (LVR) decreases. This gives you more bargaining power and access to better deals.

Changing Financial Needs: Maybe you’ve had a baby, changed jobs, or want to renovate. Your original loan might not be flexible enough for your new lifestyle.

The potential savings from a refinance home loan Australia strategy depend on your loan size and the difference in interest rates.

Let’s look at a hypothetical example.

Imagine you have a $500,000 mortgage with 25 years remaining at an interest rate of 6.50%.

If you find a best refinance home loan offer at 5.90%:

Note: These figures are examples only. You should always consult with a professional to calculate savings specific to your situation.

Refinancing doesn’t have to be a headache. Here is the standard path for home loan refinancing.

Check your current interest rate, fees, and whether you are paying for features you don’t use. Look at your exit fees or “break costs” if you are on a fixed rate.

Don’t just look at the headline rate. Look at the comparison rate, which includes fees. This gives you a truer picture of the loan’s cost.

Your new lender will need to value your property to confirm how much equity you have. In many cases, this is done electronically and costs you nothing.

You will need to provide updated payslips, bank statements, and ID. This is where mortgage refinancing tips from a broker come in handy—they handle the paperwork for you.

Once approved, your new lender arranges to pay out your old lender. The title of your property is transferred to the new bank, and your new repayments begin.

While the goal is to save money, switching lenders isn’t always free. It is vital to weigh the upfront costs against the long-term savings when you refinance home loan Australia.

Discharge Fees: Your old lender may charge a fee to close your loan (typically $200–$400).

Break Costs: If you refinance mortgage Australia fixed-rate loans before the fixed term ends, you may face significant break costs

Application Fees: New lenders may charge a fee to set up the loan, though many will waive this to win your business.

Valuation Costs: Some lenders charge for the property valuation, while others absorb this cost.

Government Fees: There may be small mortgage registration fees required by the state land titles office.

When searching for a lower home loan interest rate or the best refinance home loan, you will need to choose between fixed and variable rates.

Fixed Rate Benefits: You lock in an interest rate for a set period (e.g., 1-5 years). This provides certainty regarding your repayments, which is great for budgeting.

Variable Rate Benefits: The rate can move up or down with the market. Variable loans often come with more features like offset accounts and the ability to make unlimited extra repayments.

For many NSW homeowners, a “split loan” (part fixed, part variable) offers the best of both worlds.

You can go directly to a bank, but you will only see their specific products. Working with a home loan broker Marayong based expert like A2Z Finance Australia gives you access to the whole market.

Access to Multiple Lenders: Brokers have access to dozens of lenders, including those that don’t advertise on TV.

Better Rates: Brokers often have access to special rates or can negotiate pricing discounts that you can’t get as an individual

Faster Approvals: Brokers know exactly what each bank requires, ensuring your application is structured for a fast approval.

Local Sydney Expertise: A local broker understands the specific property market in Sydney and Marayong.

The strategy for mortgage refinance Australia differs depending on whether you live in the property or rent it out.

Owner-Occupied Loans: Lenders generally offer their lowest interest rates to owner-occupiers because they are viewed as lower risk.

Investment Loan Refinancing: Investors looking to refinance home loan NSW properties often focus on maximizing tax deductibility. Refinancing can help release equity to use as a deposit for a subsequent investment property.

Tax and Equity Benefits: Refinancing an investment loan correctly can help structure debt to maximize negative gearing benefits (always consult your accountant).

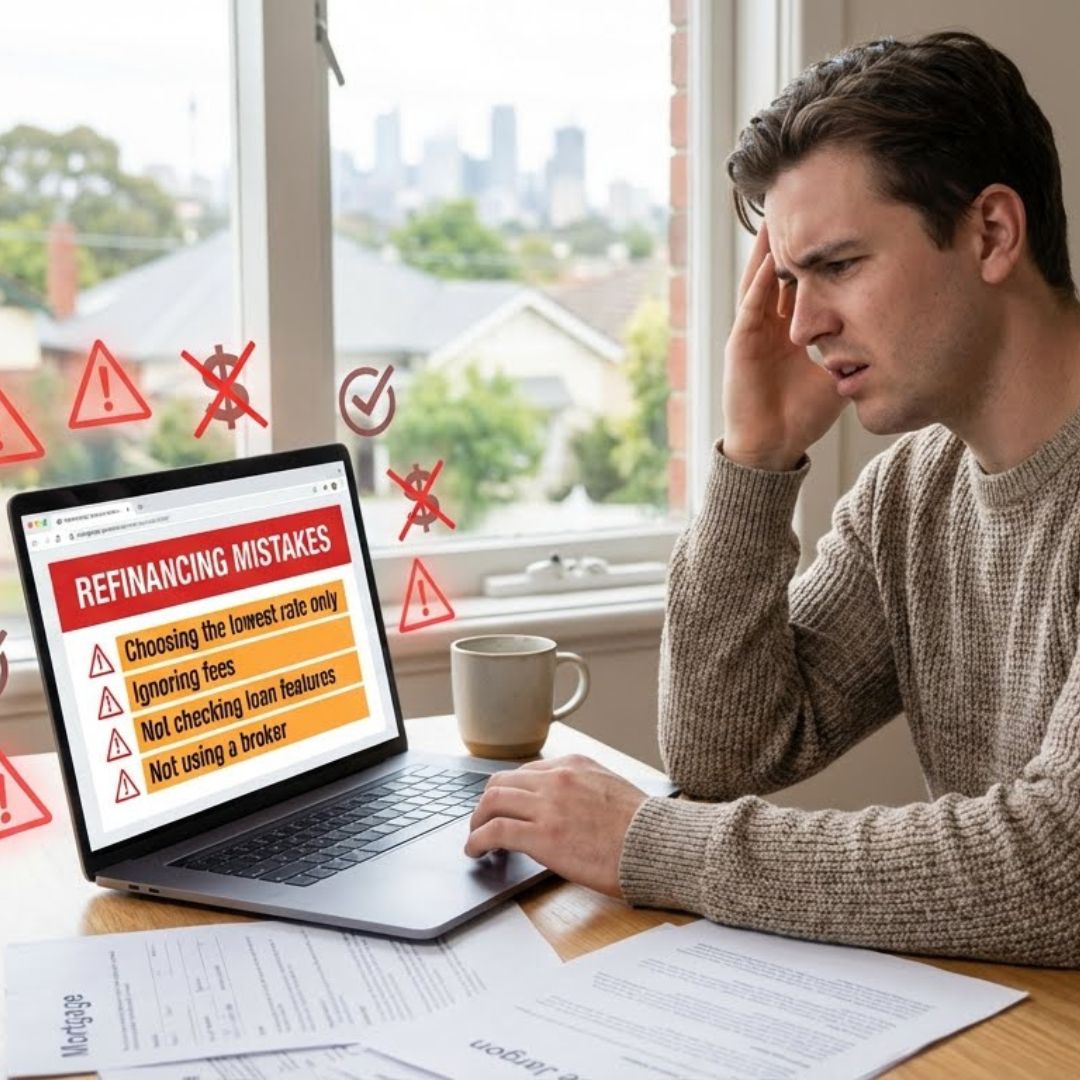

To ensure your home loan refinancing is successful, avoid these common traps:

Choosing the lowest rate only: A low rate with high ongoing fees (like a monthly service fee) might end up costing you more than a slightly higher rate with zero fees.

Ignoring fees: Always calculate the “switch cost.” If it costs you $1,000 to switch but you only save $20 a month, it will take over 4 years to break even.

Not checking loan features: Giving up an offset account to get a slightly lower rate could cost you money if you have significant savings sitting in the bank.

Not using a broker: Going it alone limits your options. Mortgage refinancing tips from a professional can prevent you from applying with a lender who is likely to decline you.

At A2Z Finance Australia, we don’t just find you a loan; we find you a solution. Whether you want to refinance mortgage Sydney properties or buy your first home, our process is designed around you.

We review your current financial health to ensure refinancing is actually in your best interest.

We compare hundreds of products to find the refinance home loan Australia options that fit your goals.

We handle the discharge forms, the new application, and the settlement process.

We stay in touch to ensure your loan remains competitive years down the track.

Don’t let rising interest rates dictate your financial future. If you want to explore how to refinance mortgage Sydney or home loan broker Marayong services can help you, the team at A2Z Finance Australia is here to help.

Contact us today for a free, no-obligation loan review and find out how much you could save.

a2z finance australia home loan home loan in marayong Home Loan Rates in Australia mortgage broker sydney refinancing home loan sydney home loans

Need help? Our team is just a message away